Real-Time Options Greeks Dashboard with AI-Powered Analysis

Build a live Greeks dashboard and ask Claude what to do before you log off.

May 21 2026

glow 574225.png "A futuristic trading dashboard floating in space showing Greek letters (Δ, Γ, Θ) glowing against a starfield")

The week before a long weekend is when positions can surprise you. Liquidity drops, bid-ask spreads widen, and that gamma exposure you've been ignoring suddenly matters. Before you step away for Memorial Day, you need to know your risk, and what to do about it.

This post builds a real-time options Greeks dashboard that monitors your portfolio's delta, gamma, theta, and vega as the underlying price ticks. Then it connects Claude to your data so you can ask questions in plain English: "What's my biggest risk going into the weekend?" or "How do I get delta-neutral?"

This post uses Claude Desktop, but Cursor, Windsurf, and any other MCP-compatible agent work identically.

Build a live Greeks dashboard, then connect Claude to ask questions about your risk in plain English.

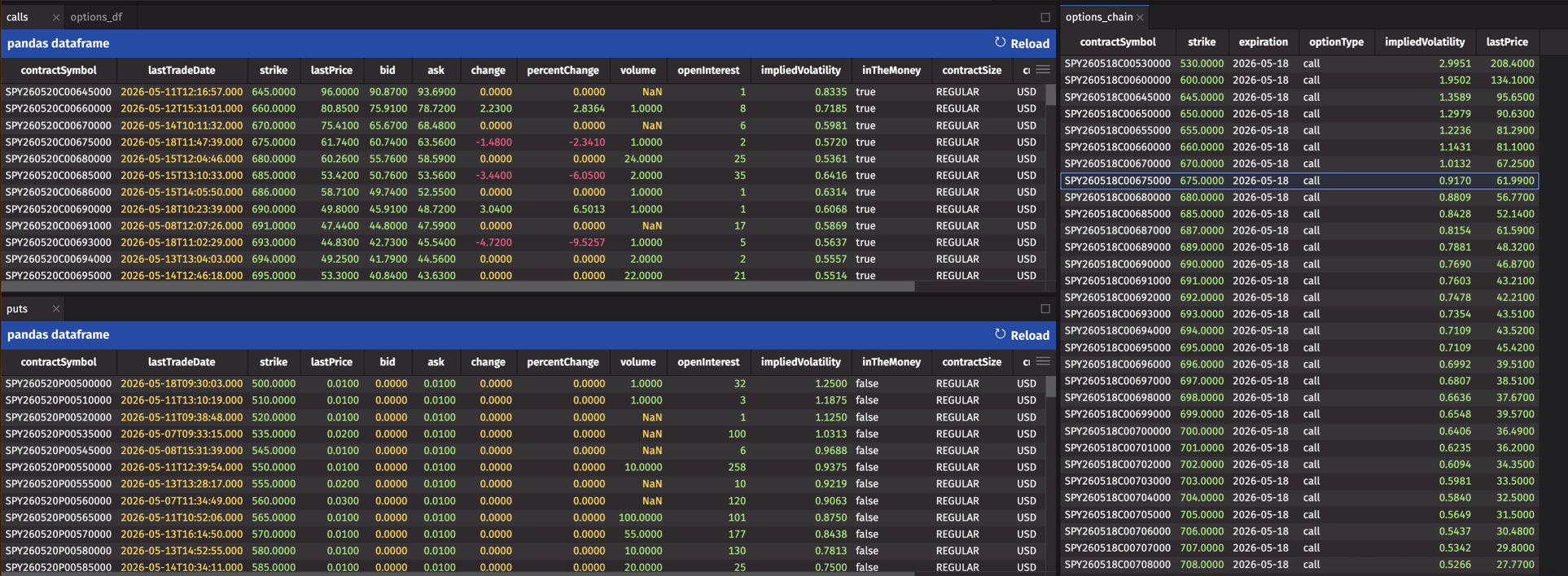

Loading the options chain

We'll pull a real SPY options chain from yfinance to get realistic strikes, expirations, and implied volatilities. Then we'll simulate the underlying price movement for the real-time demo.

Note

The code in this post runs in a Deephaven console. If you don't have Deephaven running yet, see the quickstart guide. Once it's running, install yfinance:

After installing yfinance, import it in your Deephaven console:

This gives us a realistic options chain with actual strikes, IVs, and expirations. In production, you'd replace yfinance with your live data feed.

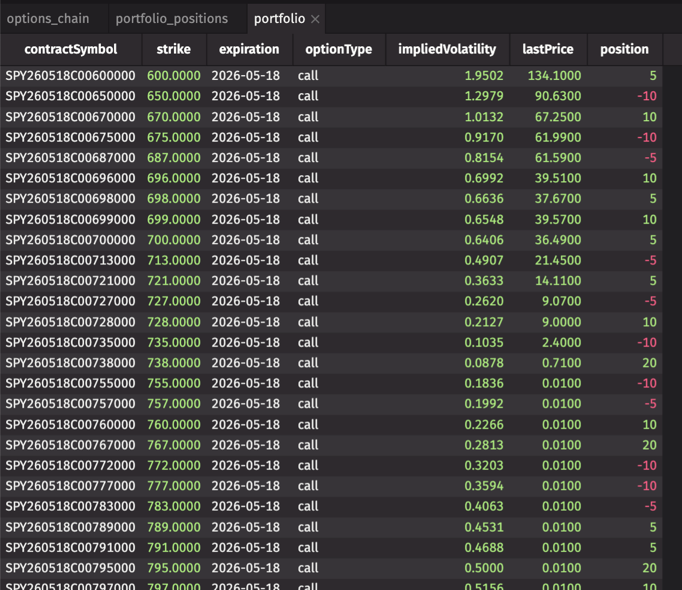

Now let's add a simulated portfolio with position sizes.

For readers who want to run this without yfinance, here's a self-contained version with synthetic data:

Click to expand: Self-contained synthetic options chain

Simulating the underlying price

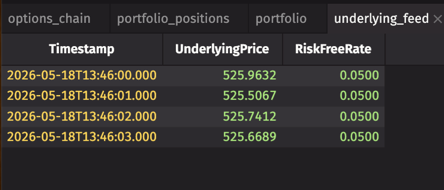

For the real-time demo, we'll use time_table to simulate the underlying price ticking every second. In production, this would be your market data feed.

Note

If you loaded real SPY options above, replace 525.0 with current_price so the simulated spot matches your strikes.

This creates a ticking price feed that updates every second. The sine wave simulates intraday price movement, and the Gaussian noise adds realistic volatility. Every time the price ticks, our Greeks will recalculate.

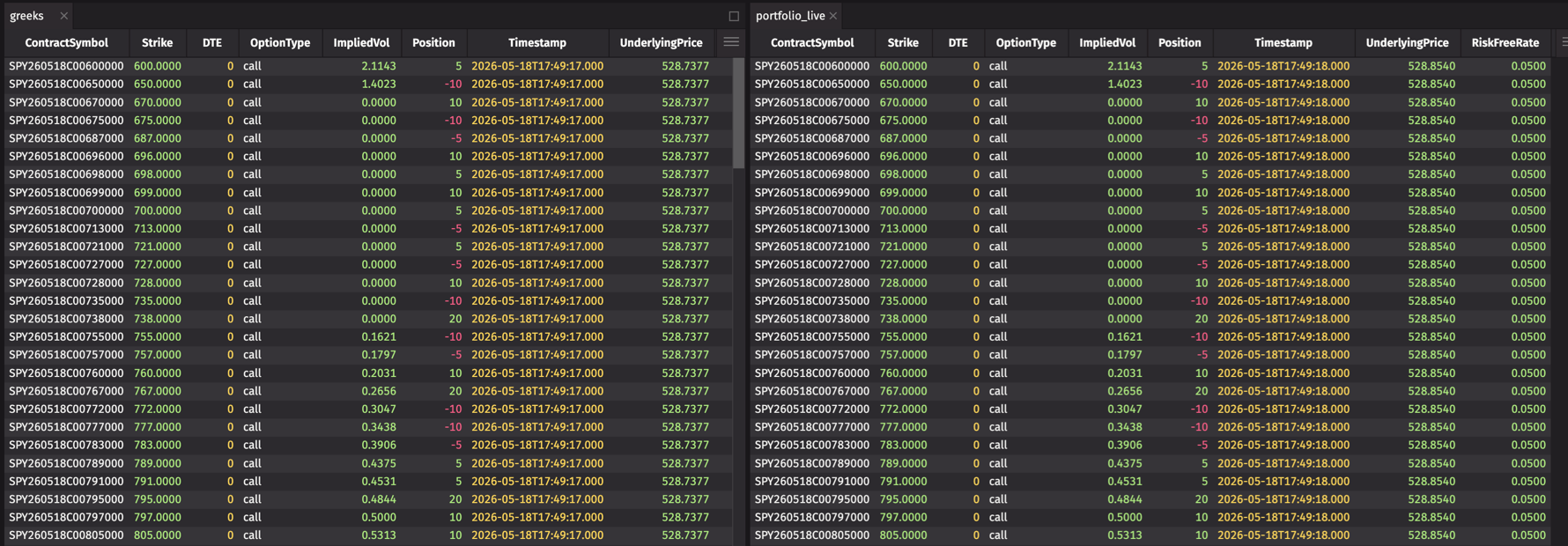

Calculating Greeks in real-time

Now for the core of the dashboard: Black-Scholes Greeks that recalculate every tick. We'll use update_view to define formula columns — efficient because they don't copy data, and they recalculate automatically when the underlying price updates.

Each Greek updates automatically when the underlying price ticks. The formulas use the Abramowitz & Stegun polynomial approximation for the normal CDF, accurate to ~7.5×10⁻⁸ — more than sufficient for risk monitoring.

Greeks recalculate every tick. No refresh button. No stale data.

Portfolio-level risk

Individual position Greeks are useful, but you need the portfolio view. Let's aggregate to see your total delta, gamma, theta, and vega exposure.

This gives you the numbers that matter: total delta (shares equivalent), gamma (how fast delta changes), theta (daily decay), and vega (IV sensitivity).

Weekend theta

A 3-day weekend means 3 days of theta. If you're short options, that's decay you collect. If you're long, that's bleed.

If your weekend theta is deeply negative, you're paying to hold. Consider whether the position is worth the bleed.

Let's also break down exposure by expiration to see where risk is concentrated.

If your near-term expirations are showing outsized gamma, that's your weekend risk. Gamma accelerates as expiration approaches, and a gap open Tuesday morning could move your P&L fast.

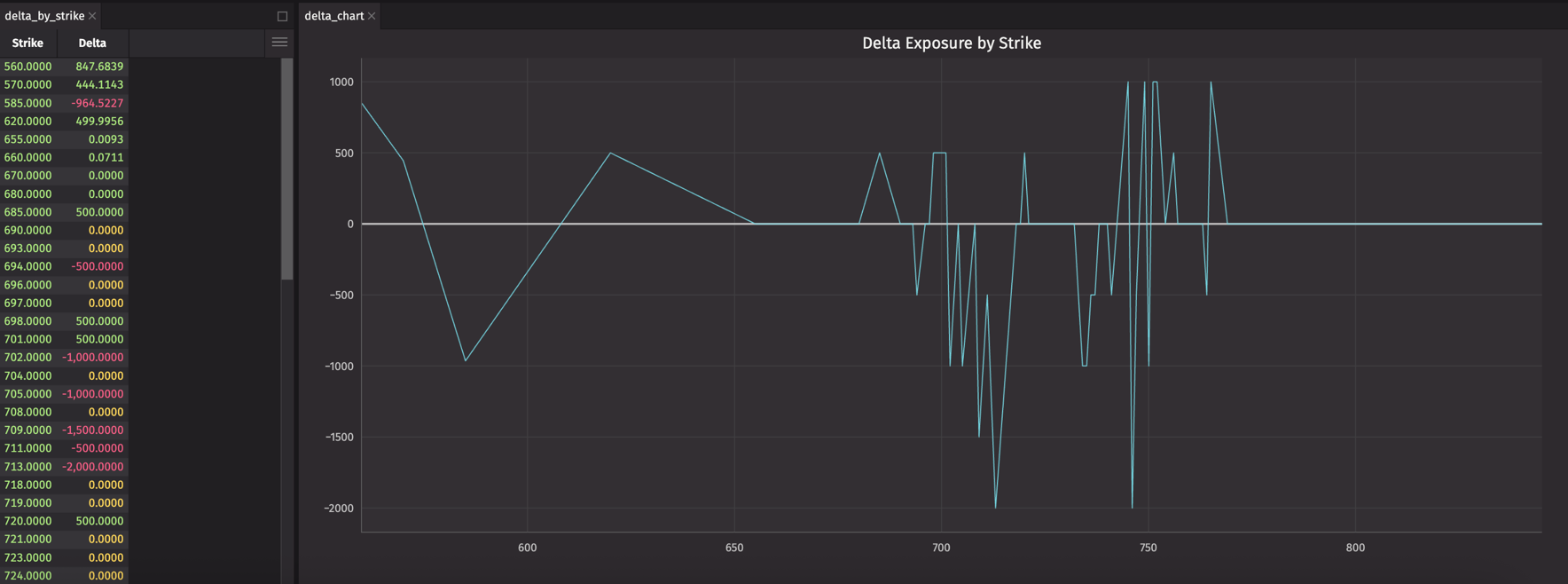

Delta by strike

A chart makes the risk intuitive. Let's see where your delta is concentrated across strikes.

Long delta clustered around ATM strikes? Positive delta from short puts at lower strikes? The chart shows it at a glance.

Scenario analysis

"What's my delta?" isn't enough. You need to know what happens if SPY gaps 3% Tuesday morning. Let's calculate P&L for different price moves using the delta-gamma approximation: P&L ≈ Delta × ΔS + ½ × Gamma × ΔS².

This tells you your downside before you step away. A 3% gap (about 15 points on SPY) could move your P&L sharply in either direction — the gamma convexity helps on the upside.

Connecting Claude to your data

With Greeks updating in real-time, the next step is connecting Claude so you can ask questions about your risk in plain English.

The connection runs through MCP (Model Context Protocol), an open standard for linking AI assistants to external tools.

Install the MCP bridge

Configure Claude Desktop

Open ~/Library/Application Support/Claude/claude_desktop_config.json (macOS) and add:

Create deephaven_mcp.json:

If you launched Deephaven with anonymous auth, set "auth_type": "Anonymous" and omit auth_token. Full configuration options are in the MCP setup guide.

Restart Claude Desktop after saving. For Cursor, Windsurf, or other agents, see the MCP setup guide for per-tool config steps.

Asking questions about your risk

With MCP connected, you can ask Claude about your options exposure in plain English.

Caution

The examples below are illustrative, not trading advice. AI can misinterpret data, make calculation errors, or miss context that affects your actual risk. Always verify recommendations before executing trades.

"What happens if SPY gaps down 3% Tuesday morning?"

Claude: I'll calculate your P&L using the scenario analysis table. A 3% gap at current prices is about a 15-point move.

That's a meaningful loss on a gap down that size. Your long delta hurts on the way down, but the gamma cushions it slightly. The bigger question: is that loss acceptable, or should you hedge before the weekend?

"Should I hedge with shares or reduce positions?"

Claude: Let me compare the two approaches. First, the share hedge:

Selling shares neutralizes delta but keeps your gamma exposure. You're still exposed to a gap, just not directionally. Closing positions eliminates both delta and gamma but realizes any P&L and may have wider spreads on Thursday afternoon.

If you're worried about a gap specifically, consider closing some of the 7-DTE positions where gamma is concentrated. If you just want directional neutrality, the share hedge is cleaner.

"What's my weekend theta?"

Claude: I'll pull your 3-day theta exposure.

That's your cost of carry for the weekend. If you're net short options, you're collecting that. If you're net long, you're paying it. Compare that to your scenario P&L — is the theta bleed worth the gamma exposure you're holding?

"Which positions should I close before the weekend?"

Claude: I'll rank positions by risk contribution — gamma for gap risk, theta for bleed.

These near-term positions carry the most gamma. Closing any of them reduces your gap risk. The tradeoff: you're also giving up their theta and any directional view you have.

Ask Claude what you'd ask a risk manager: "What happens if we gap?" "Should I hedge or reduce?" The data is live, and so are the tradeoffs.

The bottom line

Before you step away for the long weekend:

- Know your downside. The scenario table shows P&L for different gap sizes. If a 3% move wipes you out, hedge.

- Know your theta. Weekend theta is 3 days of bleed (or collection). Make sure it's worth holding.

- Know your tradeoffs. Share hedges are clean but keep gamma. Closing positions eliminates risk but may cost more in spreads.

Every calculation updates live. As the underlying ticks, your Greeks recalculate. And because Claude is connected to your live data, you can ask follow-up questions as the market moves — not just "what's my delta?" but "should I hedge or reduce?"

Try it yourself:

- Run this dashboard in your browser (Deephaven demo).

- Install locally to connect your own data (Quickstart).

- Connect Claude via MCP.

- Pull your actual positions, point the underlying feed at your market data, and ask Claude what you should do before you log off.

Join the conversation on Slack — the market doesn't wait, and neither should your risk monitoring.